SBI Fixed Deposit 2026: For investors who prefer stability over uncertainty, fixed deposits continue to be one of the most trusted financial tools in India. In 2026, fixed deposits from State Bank of India remain a popular choice for individuals looking to grow their savings without market risks. Whether you are investing ₹50,000 or up to ₹5 lakh, SBI FD offers predictable returns, flexible tenures, and peace of mind.

If you are planning to park your money safely and want to understand how much you can earn, this guide will help you calculate returns easily and make better decisions.

Why SBI Fixed Deposit Remains a Safe Choice

Fixed deposits are considered one of the safest investment options because they are not linked to stock market performance. SBI, being India’s largest public sector bank, adds an extra layer of trust and reliability.

SBI Fixed Deposit 2026 The bank offers guaranteed returns, meaning you know exactly how much you will earn at the time of investment. This makes it ideal for conservative investors, retirees, and those who want to preserve their capital.

In 2026, SBI FD continues to attract investors due to competitive interest rates and flexible investment options.

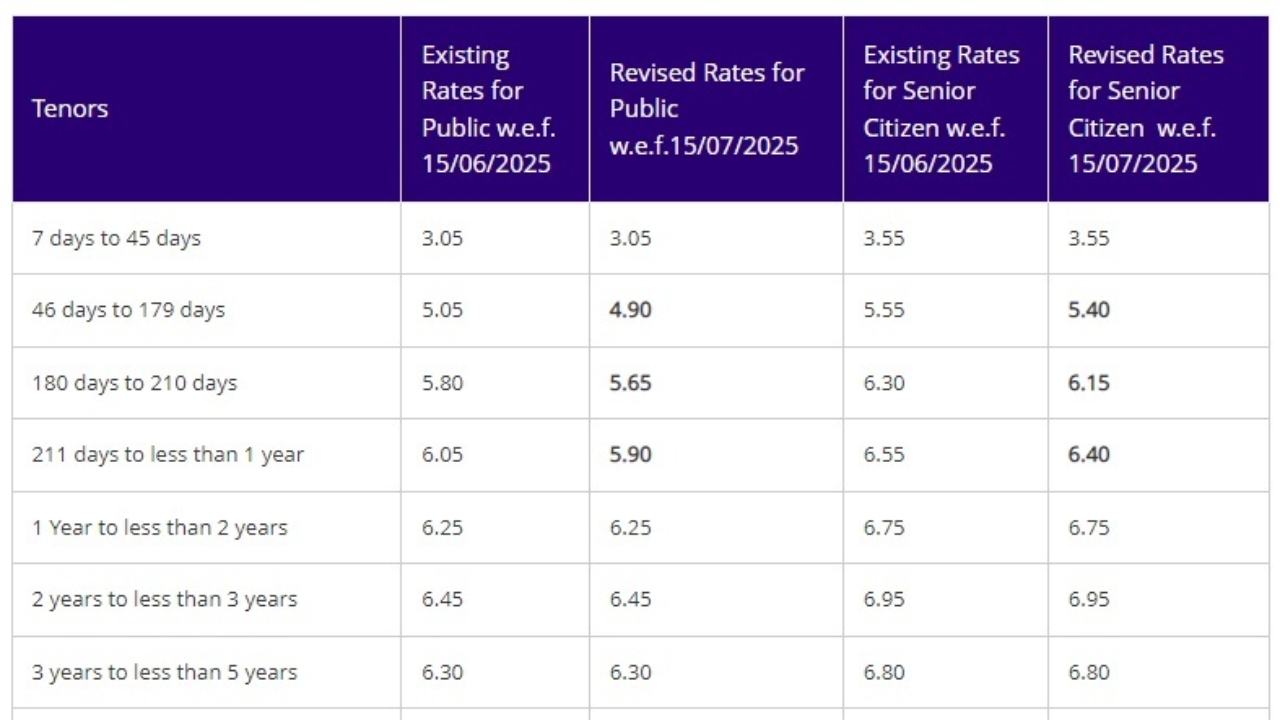

SBI FD Interest Rates in 2026

Interest rates for SBI fixed deposits vary depending on tenure. Typically, rates range between 5.5% to 7.5% per annum for general citizens, while senior citizens receive slightly higher rates.

Here is a general idea of how rates are structured:

- Short-term deposits (1–2 years): Around 6%

- Medium-term deposits (2–5 years): Around 6.5% to 7%

- Long-term deposits (5+ years): Up to 7.5%

These rates may change periodically, but the key advantage is that once you lock your FD, your rate remains fixed for the entire tenure.

Returns on ₹50,000 Investment

Let’s start with a smaller investment to understand the earning potential.

If you invest ₹50,000 for 3 years at an average interest rate of 6.8%, your returns would look like this:

- Interest earned ≈ ₹10,800

- Maturity amount ≈ ₹60,800

This shows that even a modest investment can grow steadily without any risk.

Returns on ₹1 Lakh Investment

For a ₹1 lakh investment over 5 years at around 7% interest:

- Interest earned ≈ ₹40,000

- Maturity amount ≈ ₹1,40,000

This is where the power of compounding starts to show. The longer you stay invested, the better your returns.

Returns on ₹3 Lakh Investment

If you invest ₹3 lakh for 5 years at 7%:

- Interest earned ≈ ₹1,20,000

- Maturity amount ≈ ₹4,20,000

This level of investment is ideal for individuals saving for mid-term goals such as education, travel, or a planned expense.

Returns on ₹5 Lakh Investment

For a larger investment of ₹5 lakh over 5 years:

- Interest earned ≈ ₹2,00,000

- Maturity amount ≈ ₹7,00,000

This makes SBI FD a strong option for those who want safe wealth accumulation without taking risks.

Types of SBI Fixed Deposits

SBI offers multiple FD options to suit different financial goals:

- Regular Fixed Deposit: Standard plan with fixed tenure and interest

- Tax Saving FD: 5-year lock-in with tax benefits under Section 80C

- Flexi Deposit: Linked to savings account for better liquidity

- Senior Citizen FD: Higher interest rates for individuals above 60

Each type caters to different needs, whether it is tax saving, liquidity, or higher returns.

Tenure Flexibility and Investment Planning

One of the biggest advantages of SBI FD is its flexible tenure, ranging from 7 days to 10 years. This allows you to align your investment with your financial goals.

Short-term FDs are suitable for emergency funds or temporary parking of money. Long-term FDs work well for retirement planning or future financial security.

Many investors also use the laddering strategy, where they invest in multiple FDs with different maturities to maintain liquidity and optimize returns.

Taxation on SBI Fixed Deposit

Interest earned from fixed deposits is taxable under your income tax slab. If your interest income exceeds the prescribed limit, TDS (Tax Deducted at Source) is applicable.

To manage taxes efficiently, investors often split deposits across family members or use tax-saving FDs.

It is important to calculate post-tax returns to understand the real earnings from your investment.

Premature Withdrawal and Loan Facility

SBI FDs offer liquidity options in case you need funds before maturity.

Premature withdrawal is allowed with a small penalty on interest. Additionally, you can take a loan against your FD, usually up to 90% of the deposit amount.

This ensures that your investment remains useful even during financial emergencies.

Who Should Invest in SBI FD?

SBI Fixed Deposits are best suited for:

- Risk-averse investors who prioritize safety

- Retirees looking for stable income

- Individuals saving for short to medium-term goals

- People who want guaranteed returns without market exposure

However, younger investors seeking high growth may need to combine FDs with other investment options like mutual funds or equities.

Key Advantages of SBI Fixed Deposits

- Guaranteed returns with zero market risk

- Flexible investment tenure

- Wide range of deposit options

- Easy online and offline account opening

- Loan facility against FD

These features make SBI FD a reliable choice for millions of investors across India.

Limitations You Should Consider

- Returns may be lower compared to inflation over long periods

- Interest income is fully taxable

- No high-growth potential like equity investments

Understanding these limitations helps in building a balanced portfolio.

Conclusion

SBI Fixed Deposit in 2026 continues to be a dependable investment option for those who value safety and predictability. Whether you invest ₹50,000 or ₹5 lakh, the scheme offers stable returns, flexible tenures, and complete peace of mind.

While it may not deliver high returns like market-linked investments, its strength lies in consistency and capital protection. For many investors, especially those looking for secure financial planning, SBI FD remains a cornerstone of their portfolio.

Final Thoughts

Before investing, always evaluate your financial goals, risk tolerance, and tax implications. Fixed deposits work best when combined with other investment options to create a balanced and resilient financial strategy.